How do you solve the value-add equation in hotels?

In this blog, Gabriele Capacci, Hotel Consultant at Christie & Co, discusses the current hotel investment landscape and the value-add strategy scene.

Business. Built around You.

Your expert business property advisers

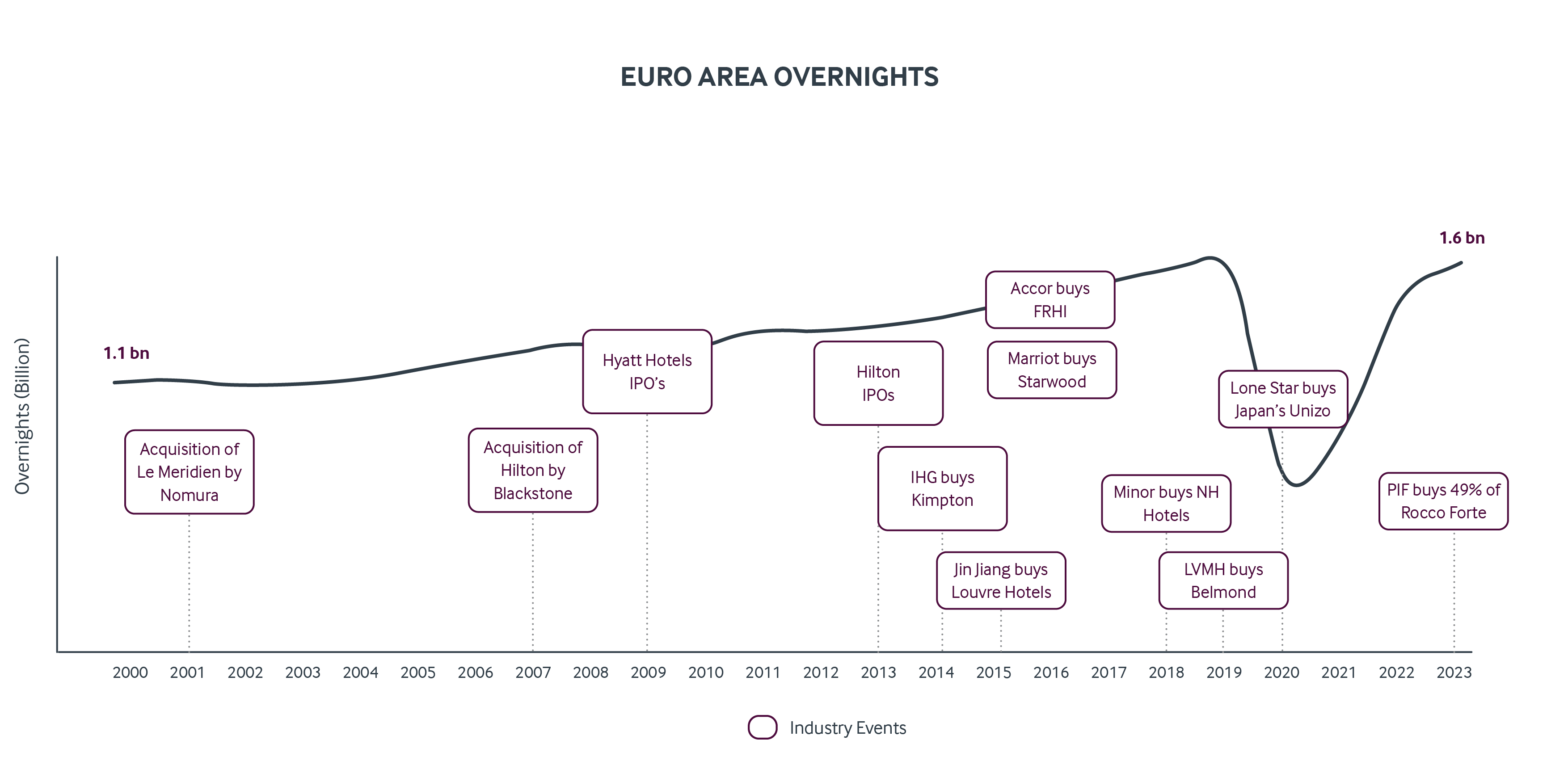

A rapidly evolving sector with growing popularity amongst investors

Historically, hotel investments were made by brands or wealthy individuals and families diversifying their portfolios. In the 1990s, major hotel brands such as Marriott and Hilton shifted to asset-light strategies, to reduce asset-heavy balance sheets and accelerate their expansion. By focusing on franchising and management contracts, these brands grew aggressively without property ownership, benefiting from revenue streams whilst maintaining strong balance sheets.

Over the past 20 years, the hotel sector has shown resilience throughout significant shocks, attracting a broader range of investors who are drawn to the diverse contractual models and risk profiles. Private Equity firms, REITs, and sovereign wealth funds have increasingly invested in hotels for high returns through value-add opportunities, and the sector’s professionalisation has attracted more interest and increased competition.

This solidifies its position as a distinct and appealing assess class within the commercial real estate market, leading to an expansion of the value-add space. In this blog, we shine a light on the current value-add strategy scene.

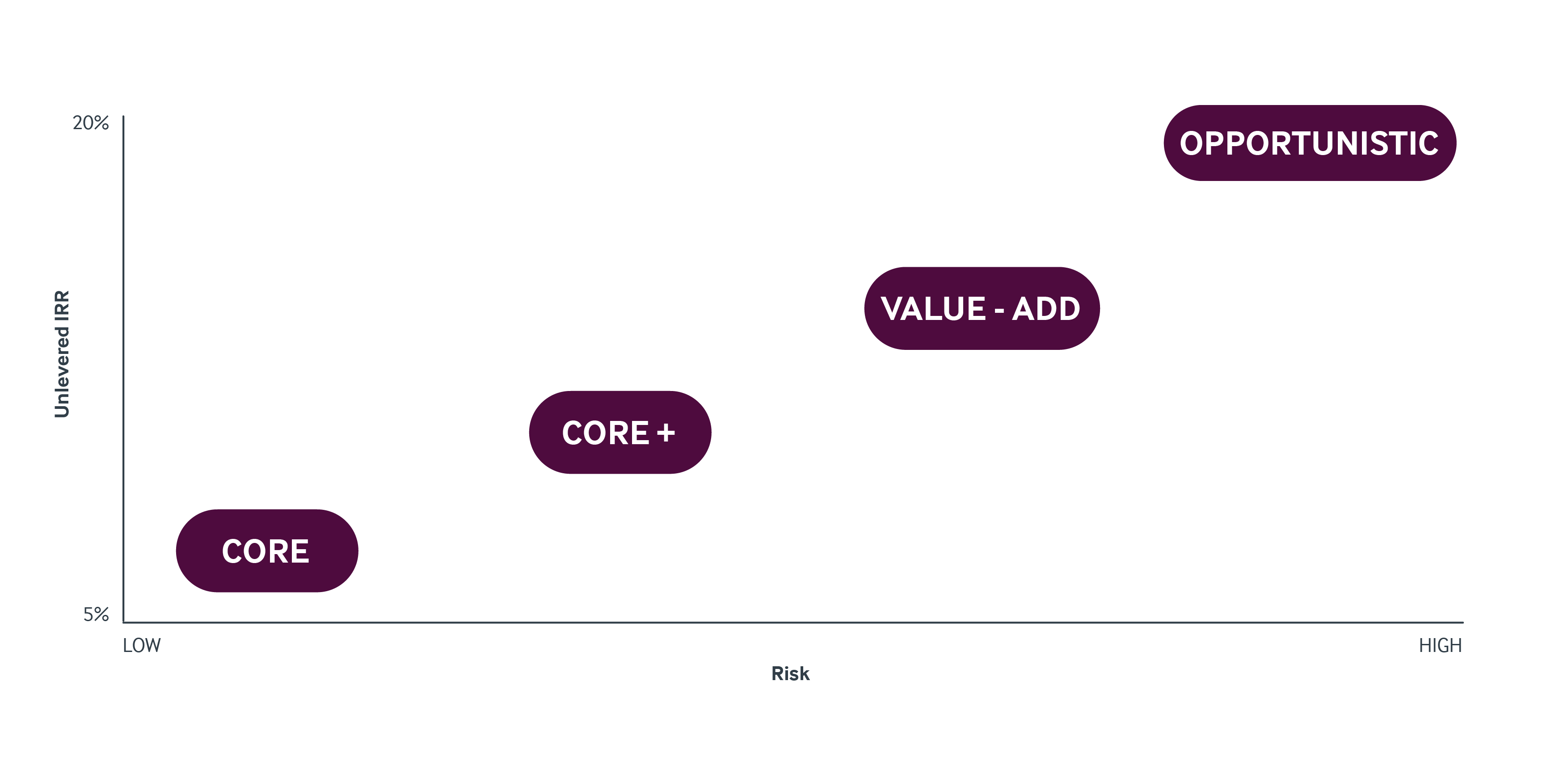

Investor profiles

Investor classification is linked to the minimum Internal Rate of Return (IRR) they require. While each investor and investment is unique, they generally fall into the following categories:

- Core Investors focus on high-quality properties, stabilised trading in prime markets with creditworthy tenants. Core investments present minimal risk and provide steady, predictable cash flows, similar to bonds. They are typically leased with a focus on fixed income, use little to no leverage and aim for returns below 8%. Holding period: Long term.

- Core + Investors seek properties that are slightly lower in quality or in good, but not prime, markets. These properties may require minor bricks and mortar and/or management improvements to enhance value. Core + investments carry moderate risk and offer higher returns than Core investments, typically around 10%-13% IRR. Holding period: medium/long term.

- Value-add Investors target properties that need significant product investment or repositioning. Value-add investments involve moderate to high risk, as they often require substantial capital for renovations or redevelopment. By driving both the property’s value and operating cash flow, IRRs between 13% and 18% are typically expected. Holding period: duration of fund (5 to 7 years).

- Opportunistic Investors pursue the highest-risk, highest-reward projects. These can include ground-up developments, major redevelopments, or turnaround of distressed properties. Opportunistic investments often involve significant capital expenditure and leverage, with the potential for substantial returns, sometimes exceeding 20%.

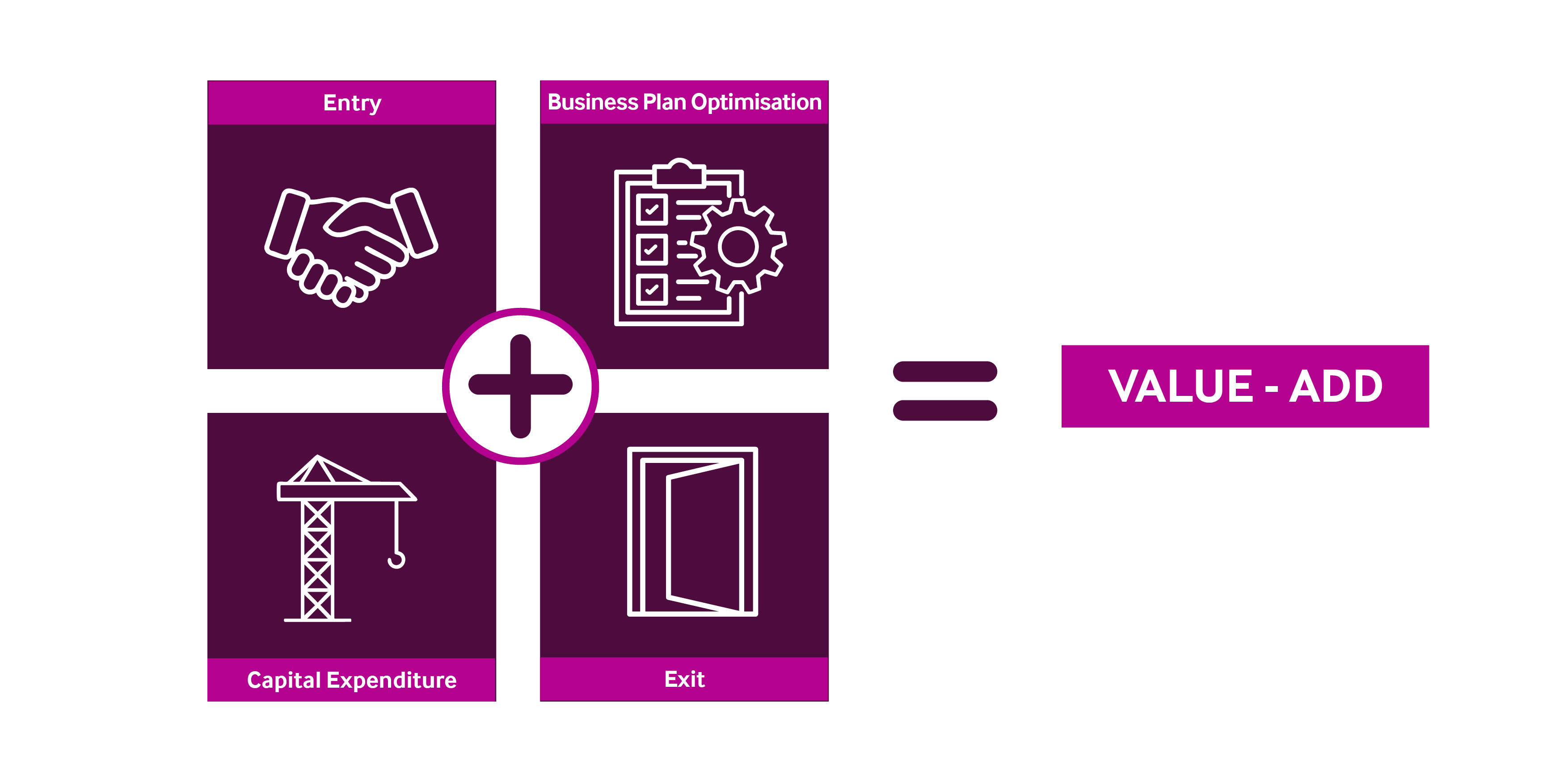

Resources and skill-based strategy

A value-add strategy actively creates value for a hotel asset through components like the acquisition price, income streams, and disposal proceeds. Investors focusing on one or more of these aspects will require different skills, resources, and capital investments, as outlined in this equation:

Let’s break the equation down:

Entry: Value is created by increasing the gap between the entry and exit yield. This involves buying the asset at a favourable price and positioning it for a higher exit yield through strategic improvements and market positioning. Enhancing the asset's appeal also broadens the exit buyer pool, increasing the premium investors are willing to pay.

Business Plan: Focus on optimising the hotel's operational EBITDA through enhanced revenues and/or cost optimisation. Other options include rebranding, space reallocation within the building, and enhancement of income streams.

Capex: The business plan and exit strategy can be further stimulated by investing in value-add or ROI projects. These projects may include renovations, upgrades to facilities, or the introduction of new amenities that attract more guests and increase the hotel's overall value.

Exit: The additional value produced at the exit stage is achieved through enhanced cash flows and improved exit yield. This can be influenced by macroeconomic or geopolitical risks, financing conditions, the timing of the disposal, and/or increased appetite in location, and a strong commercialisation process.

Value-add levers

Certain levers can be utilised to significantly enhance the outcome of this value-add equation. Here are a few examples:

Entry

- Tired asset: Properties which have been starved of capex present opportunities for acquisition below replacement cost, therefore generating value/returns from acquisition.

- Distressed seller: Sellers who are under financial pressure, such as those with leases under water, over-leveraged properties, in administration, or a need for cash for other activities, present opportunities for quick, below-market value acquisitions.

Business Plan

- Operational mismanagement: Inefficiencies in managing the hotel's operations, from revenue generation to cost control, can present opportunities for improvement in EBITDA margins.

- Operational inefficiencies: Possibility to radically change the operating strategy of the hotel, from family operations to third-party/white-label, or clustering into a portfolio of hotels, leading to the streamlining of management costs, improved sales platform and distribution visibility.

- Lack of commercial focus: Poor asset visibility and ineffective distribution channels can limit the hotel's market reach. Implementation of a brand and their commercial distribution network can increase ADR and occupancy driving bottom line performance.

- Underperforming spaces: Hotels with unique features or large meeting spaces may underperform, so improving operating strategies and realigning operational teams can help. Evolving market conditions and changing consumer behaviours can also lead to revenue shortfalls: leasing or managing these spaces through third parties can be beneficial.

- Operating structure shift: Value-add investors are able to extract value by switching a hotel from management to franchise. Alternatively, de-flagging a hotel allows investors to reposition the property, potentially attracting a different market segment and enhancing revenue through unique branding and operational flexibility.

Upside with capex

- Repositioning: Capex value-add levers are intertwined with business plan optimisations: for example, there is the possibility with capital investment to reposition the property within its market, driving a new commercial strategy.

- Extension potential of rooms: Opportunities to add more rooms to the existing hotel structure therefore drive room count and possibility to yield on high occupancy days.

- Addition of other facilities: The potential to activate “underused” spaces which might have required high capital amounts for previous owners can drive real estate value and operational efficiency.

- ESG: There is the potential for significant upside in maximising the ESG credentials of the real estate and driving a sharper exit yield (green premium) by widening the investor pool to more institutional investors and lowering operating costs, particularly in utilities.

Summary

The value-add strategy for hotel investments is a popular topic among specialist players, and can enhance asset value through acquisition, operational improvements, and capital expenditure.

By targeting underperforming, underinvested, and distressed assets, investors can generate significant returns by repositioning and optimising operations. Timing and market identification are crucial, and here at Christie & Co our specialist hotel consultancy and brokerage teams can help investors navigate trends to capitalise on such opportunities in an increasingly popular property asset class.